What is Export Obligation under EPCG Scheme?

EPCG scheme, as you all may know, allows duty-free import of capital goods/machinery for the production of high-quality export goods. EPCG scheme is introduced by the Government with a single aim to increase exports from India.

Therefore, by giving this concession of zero duty import, GOI is assigning a task/job to you. And your task is to increase export sales of your company after the installation of the said new machinery in comparison to earlier sales. This task/job assigned to you by the GOI is known as an export obligation. The export obligation under the EPCG scheme is compulsory and does not come with a choice. DGFT has the right to take action against any exporter who does not fulfil the export obligation. Including non fulfillment of export obligation under EPCG.

Watch this short introductory video on the EPCG Scheme; which explains the complex concept of EPCG in an easy to understand manner. It Explains What is EPCG Scheme and its application process; details about Export obligation & Redemption of EPCG License; entire summary and step by step procedures involved in the EPCG scheme.

EPCG Export Obligation

- In the EPCG Scheme, the Export Obligation period is of 6 years.

- Export Obligation is fulfilled by the authorisation holder only by exporting goods, which are manufactured using the said machinery. Export obligation cannot be fulfilled by the export of alternate products not mentioned on the EPCG License.

- Export obligation can be completed either by direct export, third-party export or deemed export.

- The EPCG Authorisation holder shall submit to RA concerned a report on fulfilment of export obligation through online mode after expiry of first block period of four years and continuously till the expiry of valid EO period.

- Shipping Bills containing details of Advance Authorisation, DFIA, MEIS, Drawback or any other reward scheme can be counted in Export Obligation fulfilment only if EPCG License details are mentioned in it.

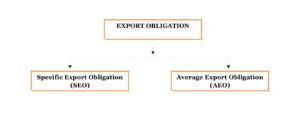

Export Obligation imposed in the EPCG Scheme is of two types:

Types of Export Obligation under EPCG Scheme

Let us understand each export obligation type in detail.

Specific Export Obligation (SEO)

Under Specific export obligation, an exporter has to export goods equal to 6 times of the actual duty saved amount within 6 years starting from the EPCG license issue date.

In SEO, the Export Obligation should be completed block-wise:

- 1st Block: The first four years from the issue of the license is said as 1st block and in this block, the exporter has to complete a minimum 50% of the Export Obligation.

- 2nd Block: The last two year i.e. 5th and 6th year from the issue of the license are said as 2nd block and in this block, the exporter has to complete the remaining Export Obligation.

If the Authorisation holder fails to fulfil the 1st block, he can extend the Blockwise EO by paying composition fees as mentioned below:

As per Para 5.13 ( c) of PN 15 /2024-25 dated 25 .07.2024 , authorization holder can request RA for extension of Export Obligation period of first block in 3 ways:

1. If the EPCG Authorisation holder submits the request within 6 months from the date of expiry of first block EO period then the composition fees will be as under

| Duty Saved Value of EPCG Authorization issued | Composition Fee to be levied (in Rupees) |

|---|---|

| Up to Rs.2 Crores | Rs.5,000 |

| More than Rs. 2 Crores to Rs. 10 Crores | Rs.10,000 |

| Above Rs.10 Crores | Rs.15,000 |

2.RA may consider the request for extension of block-wise EO period, received after 6months but within 6 years from date of issue of authorization, with composition fee as under:-

| Duty Saved Value of EPCG Authorization issued | Composition Fee to be levied (in Rupees) |

|---|---|

| Up to Rs.2 Crores | Rs.10,000 |

| More than Rs. 2 Crores to Rs. 10 Crores | Rs.20,000 |

| Above Rs.10 Crores | Rs.30,000 |

3.RA may consider the request, if the application is made beyond 6 years , for extension of block-wise EO period for regularization purpose with composition fee as under:-

| Duty Saved Value of EPCG Authorization issued | Composition Fee to be levied (in Rupees) |

|---|---|

| Up to Rs.2 Crores | Rs.15,000 |

| More than Rs. 2 Crores to Rs. 10 Crores | Rs.30,000 |

| Above Rs.10 Crores | Rs.45,000 |

Average Export Obligation (AEO)

- In Average Export Obligation (AEO), the average turnover of same & similar products maintained in the preceding three financial years before the license issued should be maintained in each financial year until we fulfill the Specific Export Obligation (SEO).

- In this obligation, the DGFT wants you to maintain the export performance you already achieved in previous financial years.

As already discussed, the EPCG scheme is introduced with the objective to increase exports, therefore AEO makes sure the average is maintained and SEO makes sure that there is an increase in exports.

This aligns with India’s commitment to facilitating trade through schemes that support consistent export performance and align with World Customs Organization (WCO) and framework of standards to secure and facilitate global trade.

EPCG Export Obligation Calculation

Let us understand the calculation of export obligation under the EPCG scheme with the help of an example:

Let’s say Company ABC Pvt. Ltd. is engaged in international trade of “Toothbrushes” and are going to import CNC tufting machine which binds Toothbrush handles with Bristles. They took the EPCG License of CIF value which is approximately 38,000 USD and below is the table for calculating Duty saved value.

- As per the above, the duty saved value is 8,26,560 INR i.e. the duty that they saved while importing the capital goods.

- The specific export obligation is calculated as 6 times of duty saved value i.e. 8,26,560 *6 =49,59,360 INR to be completed in 6 years.

- They applied for the license in F.Y. 2020-21, therefore to calculate the AEO, they have to check export turnover of “Toothbrush” for previous three F.Y. i.e. 2019-20, 2018-19, 2017-18. Suppose average comes out to be 1 Cr.

- So, Total export obligation is – They have to export “Toothbrushes” worth 49,59,360 INR in 6 years and also maintain 1 Cr annual export of toothbrush for all 6 years.

Extension of EPCG Export Obligation

If An Authorisation holder fails to fulfill the Export Obligation in a given period of 6 years, then he/she can extend the Export Obligation period.

- Request Period to DGFT:

- The Authorisation Holder can request DGFT RA, before 90 days from the date of the expiry of the actual Export Obligation period. Also, the RA accepts the request for extension up to 180 days with an additional composition fee of Rs. 5,000/-

- Regarding Extension:

- The DGFT RA can provide two extensions of one year each and have to pay a composition fee of 5% in the first year and 10% in the Second year respectively of proportionate duty saved value depends on unfulfilled Export Obligation.

- The minimum composition fee will be Rs. 10,000.

- Automatic Export Obligation extension on the occurrence of Ban on export Product:

- As per Para 5.20 FTP 2015-20, if there is a ban of an export product after issuance of the license, then the Export Obligation is extended automatically for a period equal to the period of the ban. The Authorisation holder is not required to maintain the average export obligation for the ban period.

- As per Para 5.16 (b) of PN 15 /2024-25 dated 25 .07.2024 ,In case of extension of Export Obligation beyond 6 years, two extensions, from date of expiry, of one year each or two years on one go at the choice of authorization holder, may be considered by RA,concerned with composition fee.

Duty Saved Value of EPCG Authorization issued Composition Fee to be levied (in Rupees) Up to Rs.2 Crores Rs.20,000 More than Rs. 2 Crores to Rs. 10 Crores Rs.30,000 Above Rs.10 Crores Rs.60,000

Penalty for Non-Fulfilment of Export Obligation

- DGFT RA may condone shortfall up to 5% in specific export obligation arising out of duty saved amount but average export obligation should be 100%.

- If the EPCG License holder fails to fulfil the average export obligation in a given period, then he is liable to pay customs duties with 15% interest per year to the customs authority.

- If the EPCG License holder has fulfiled 100 % AEO but is unable to fulfil SEO, then he is liable to pay proportionate duty saved amount with 15% annual interest.

- Failure in this respect may lead to non-fulfilment of export obligation under EPCG, attracting strict penalties.

Relaxation in Export Obligation under EPCG Scheme

- The DGFT has given the benefit or advantage for the exporter if the license holder has fulfiled 100% Average Export Obligation in each financial year from the license issued and 75% or more of his Specific Export Obligation in half or less than half of the export obligation period. The Authorisation holder can redeem the license. No need to fulfil the remaining 25% SEO.

- Relief in Average Export Obligation (AEO)

- As per para 5.19 FTP 2015-20, The DGFT has given relief in average Export Obligation for the Authorisation holder, where the particular sector experiences a downfall of more than 5% in Global trade, then Authorisation holder can approach DGFT to reduce the AEO by that much percentage.

- As per para 5.19 A FTP 2015-20, If the Authorisation holder, has made excess average export obligation in one year and less in another year, then it can be combined if the overall average export obligation is maintained.

- Our government has given an exemption to the authorization holder in maintaining the average export obligation for the given export products:-

- Handicrafts

- Handlooms

- Cottage & Tiny sector

- Agriculture

- Aqua-culture (including Fisheries), Pisciculture

- Animal husbandry

- Floriculture & Horticulture

- Poultry

- Viticulture

- Sericulture

- Carpets

- Coir and

- Jute

Incentives for Early Fulfilment of Export Obligation

Under the EPCG scheme’s there is provision of fast-track , if an exporter fulfills 75% or more of the specific export obligation and 100% of the average export obligation within half or less than half of the original export obligation period, the remaining export obligation is condoned, and the EPCG license gets redeemed.

Common Mistakes While Fulfilling EPCG Export Obligation

- Not maintaining block-wise export targets.

- Using machinery for non-approved products.

- Incorrect documentation for third-party exports.

- Delay in reporting to DGFT.

- Ignoring rules under non fulfillment of export obligation under EPCG which may result in penalties.

- Not submitting installation Certificate to RA in stipulated time frame

EPCG Export Obligation: Step-by-Step Fulfillment Process

- Apply for EPCG License.

- Import machinery under zero duty.

- Installation of Machines and Submission of Installation Certificate to Regional Authority (RA) of DGFT.

- Begin manufacturing approved export products.

- Maintain export records for both SEO and AEO.

- Submit annual returns and documentation to DGFT.

- Avail extension if needed and avoid non fulfilment of export obligation under EPCG.

- On successful completion, apply for redemption of license.

EPCG Export Obligation fulfilment through Third Party Exports

- The finished goods exported by third party exporter should be manufactured by EPCG License holder or supporting manufacturer where the imported capital goods are installed as per the license.

- The Authorisation holder name with license no. and Supporting Manufacturer details should be mentioned on the Shipping Bill or Bill of Export.

- BRC, GR declaration, export order, and invoice should be in the name of third party exporter.

- Additional Documents required for the discharge of Export Obligation through the third party exports are:-

- Copy of an agreement between the license holder and ultimate exporter, to export the finished goods manufactured by the authorization holder or supporting manufacturer for the fulfillment of export obligation against EPCG license.

- Evidence of having dispatched the goods from authorization Holders factory premises to the ultimate exporter/port of export i.e. ARE-1 certificate issued by Central Excise / Tax invoice for export under GST rules certified by customs verifying the export with the shipping bill no., date and license no. or Invoice containing license no., date and time of dispatch in case factory unit is not registered with GST / Central Excise.

- Lorry Receipt / Logistical proof for clarifying that the finished goods are moved from the premises of the authorization holder to the third party/port registered for export.

- A disclaimer certificate from third party exporter that the shipping bills and E-BRC utilized shall not be used in any other EPCG License for the fulfilment of Export Obligation.

[Click here to know the procedure for, “How to obtain and close the EPCG License“]

How Afleo Consultant can help you?

Afleo Consultants can help you to close/redeem your EPCG License with DGFT. With more than 10+ Years of experience, we can also guide you with all the procedures related to the EPCG Scheme.

We are the leading Import Export (DGFT Consultant) having a client-base across India. We provide all the services related to DGFT which includes MEIS scheme, EPCG, SEIS, Advance Authorisation, DFIA, RoSCTL scheme, TMA scheme, RoDTEP scheme etc.

Please share your thoughts about the article in the comments section below.