What is Deemed Export?

Deemed exports simply mean some kind of transactions where the goods supplied do not exit India but are treated as exports under the Foreign Trade Policy (FTP) and the GST Act. As opposed to common exports, where goods are exported out of the country, deemed exports occur within India’s geospatial boundaries, provided goods are manufactured in India.

The legal provision for deemed exports is contained under:

- Foreign Trade Policy (FTP) 2015-20, Chapter 7

- Goods and Services Tax (GST) Structure, particularly Section 147 of the CGST Act, 2017.

Difference from customary export:

In conventional exports, commodities move across the national border, and usually, payment is received in a foreign currency. In deemed exports, commodities are still within India, and payment could be received in Indian Rupees (INR) or foreign exchange following RBI norms. But deemed exports are still eligible for various export incentives.

Why Was the Concept of Deemed Exports Introduced? – What is the Objective?

The concept of Deemed Exports was introduced to support domestic manufacturing by treating certain supplies within India as if they were exports, even though the goods do not leave the country. This policy measure helps ensure that domestic suppliers receive similar benefits as physical exporters.

Objective:

The primary objective of deemed exports is to provide a level-playing field to domestic manufacturers and to promote the ‘Make in India’ initiative. It ensures that Indian suppliers are not at a disadvantage compared to foreign suppliers, especially in government-backed or internationally financed projects. The Government notifies specific cases and sectors eligible for such benefits from time to time.

Examples of Deemed Exports

Deemed exports refer to transactions where goods supplied do not leave India but are still considered exports under the Foreign Trade Policy. These supplies are eligible for export benefits such as duty drawback, GST refunds, and exemptions. Below are some real-life examples:

1. Supply to Export Oriented Units (EOUs), EHTP, STP, and BTP Units

A domestic manufacturer supplying components to an Export Oriented Unit (EOU) engaged in producing electronic goods for export is making a deemed export. Though the goods remain within India, the supply supports export production and qualifies for benefits like duty drawback and GST refunds.

2. Supply under Advance Authorisation

A textile company procuring dyes and chemicals from a domestic supplier under an Advance Authorisation scheme to manufacture garments for export is engaged in a deemed export transaction. The supplier can claim a refund of the GST paid on such supplies.

[Learn More about Advance Authorisation Scheme]

3. Supply of Capital Goods under EPCG Scheme

Supplying capital goods like machinery to an exporter under the Export Promotion Capital Goods (EPCG) scheme qualifies as a deemed export. This facilitates technology upgrades for exporters, and the supplier is eligible for benefits such as GST refunds.

[Learn More about EPCG Scheme]

4. Supply to Projects Financed by Multilateral or Bilateral Agencies

Supplying goods to infrastructure projects in India funded by international agencies like the World Bank or Asian Development Bank is considered a deemed export. These projects often follow International Competitive Bidding (ICB) procedures, and suppliers can avail benefits like duty drawback and GST refunds.

5. Supply to Mega Power Projects

Supplying goods required for setting up Mega Power Projects, as specified in DGFT notifications, is treated as a deemed export. For instance, supplying equipment to a power project that has followed ICB procedures and is listed under the relevant customs notifications qualifies for deemed export benefits.

Smarter Shipping Begins Now – Discover Our Complete Digital Freight Platform.

Types of Transactions Eligible as Deemed Exports

- Supplies to Export Oriented Units (EOUs)

- Supplies to Advance Authorization holders

- Supplies to projects under bilateral/multilateral funding

- Supplies to atomic power projects

All these categories are required to follow the guidelines given by the DGFT and GST authorities.

There are a number of transactions that are classified as deemed exports under Indian trade regulations. The following are some typical examples:

Supply to Export Oriented Units EOUs / STP / EHTP / BTP:

Deemed export benefits are extended to supplies made to EOUs, STP, EHTP, and BTP units to boost export-led manufacturing.

Supply to Advance Authorisation Holder / Annual Advance License:

Supplies made under Advance Authorisation or Annual Advance License are treated as deemed exports to support duty-free procurement for export production.

Supply of Capital Goods against EPCG Authorisation:

Capital goods supplied under the EPCG scheme qualify as deemed exports, facilitating technology upgrades for exporters.

Supply to Projects Financed by UN/World Bank:

Supplies to projects financed by foreign agencies such as the United Nations, World Bank, or other bilateral/multilateral organizations are considered as deemed exports.

Supply to Nuclear Power Projects:

Supplies to nuclear projects under the conditions specified by the government are included.

Other instances as per DGFT Notifications:

Specified supplies of cement, steel, and fuel are also eligible for deemed exports, along with certain refineries and power projects as notified by the Director General of Foreign Trade (DGFT). Also Supplies of goods for projects funded by bilateral or multilateral agencies notified by the Department of Economic Affairs, Ministry of Finance under International Competitive Bidding (ICB) are also considered as Deemed exports.

Major Advantages of Deemed Exports under Indian Foreign Trade Law

Deemed exports provide a number of incentives comparable to physical exports:

1. Eligibility for Advance Authorization/DFIA

Suppliers / Manufacturers can import goods without paying customs duty under the Duty-Free Import Authorization (DFIA) and Advance Authorization schemes. This guarantees the availability of raw materials at reasonable prices, enhancing competitiveness.

2. GST Refund/Exemption on Inputs

GST charged on inputs utilized in deemed export supplies is refundable. Alternatively, in certain instances, exemption from payment of GST is permissible at the procurement point itself.

3. Deemed Export Drawback

The suppliers are entitled to claim duty drawback as per All Industry Rate of duty draw back provided no CENVAT credit has been availed by supplier of goods on excisable inputs or on Brand Rate Basis upon submission of documents evidencing actual payment of basic custom duties.

4. Refund of Terminal Excise Duty

The supplier or the recipient is eligible to claim TED Refund provided the recipient of goods does not avail CENVAT credit/rebate of such goods.

Deemed Export vs Export vs Merchant Export

Let’s make a clear difference between them:

What is Export?

Export refers to the supply of goods physically out of India’s boundaries. For instance, shipping clothes to the USA.

What is Deemed Export?

Here, no goods are exported out of India, but the supply is treated as an export for trade benefit purposes. Example: Supply of machinery to a World Bank-funded project in India.

What is Merchant Export?

Merchant export involves purchasing goods from the domestic market and exporting them without undertaking manufacturing activities. For instance, buying handicrafts from artisans and exporting them to Europe.

| Feature | Export | Deemed Export | Merchant Export |

|---|---|---|---|

| Destination | Outside India | Within India | Outside India |

| Payment Currency | Foreign currency | INR or as per RBI rules | Foreign currency |

| Goods Movement | Cross-border | Within India | Cross-border |

| GST Treatment | Zero-rated (export supply) | Refund of GST/Input Credit | Zero-rated (export supply) |

| Eligibility for Export Benefits | Yes | Yes | Yes |

Eligibility Criteria for Deemed Export Status

For a supply to be considered a deemed export:

1. Goods should not exit the country

The goods should stay in the territory of India during the transaction.

2. Transaction should be notified under FTP/GST

The supply should come under categories notified by DGFT or under the GST law specified.

3. Buyer should be eligible

The intended buyer of the goods should be eligible, e.g., an EOU, Public Sector Undertaking (PSU), or an Advance Authorization/EPCG license holder.

4. Payment in INR or according to RBI Directives

Payment for supply should be made in Indian Rupees or foreign exchange as sanctioned by the RBI.

5. Procedural Conditions for Refund Claims

Suppliers are required to fulfil procedural conditions such as documentation and time limits to avail benefits such as GST refunds, Deemed Export Drawback etc.

Deemed Exports under GST

Under GST:

- Deemed exports are not zero-rated supplies but are subject to input tax credit refund.

- A refund can be claimed by either the supplier or the recipient.

- Deemed export supplies are charged with GST at rates applicable; however, relief can be taken after supply through refund mechanisms.

Documentation required is:

- Tax invoices

- Deemed export supply certificate

- End-use certificate from the recipient

- GST refund application (Form GST RFD-01)

Recent Updates:

- CBIC notifications (like Notification No. 49/2017-Central Tax) bring clarity in refund rules and conditions.

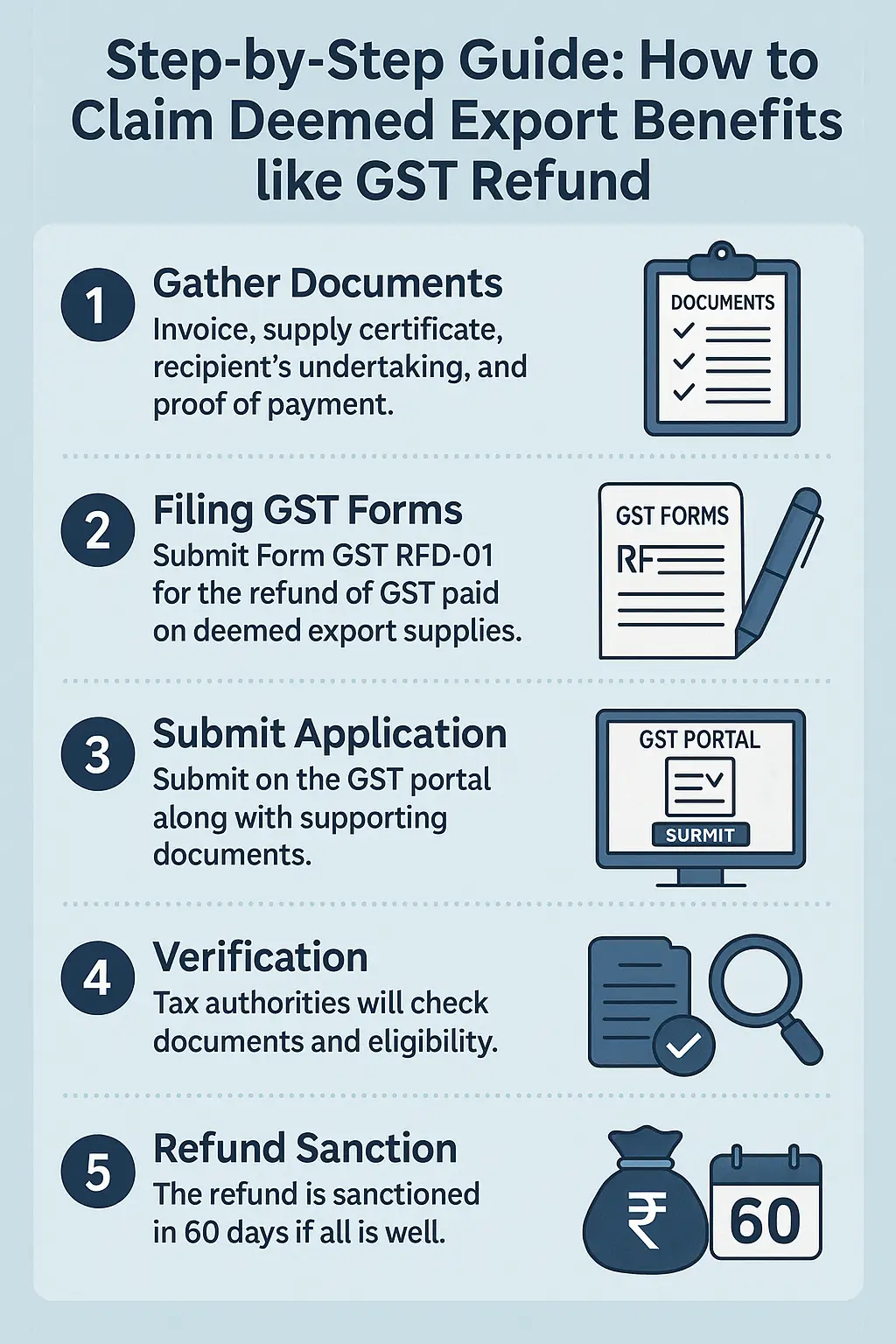

Step-by-Step Guide: How to Claim Deemed Export Benefits like GST Refund:

1. Gather Documents:

Invoice, supply certificate, recipient’s undertaking, and proof of payment.

2. Filing GST Forms:

Submit Form GST RFD-01 for the refund of GST paid on deemed export supplies.

3. Submit Application:

Submit on the GST portal along with supporting documents.

4. Verification:

Tax authorities will check documents and eligibility.

5. Refund Sanction:

The refund is sanctioned in 60 days if all is well.

Typical Challenges in Deemed Export Compliance

1. Documentation Mistakes:

Incorrect or missing certificates usually lead to delayed refunds.

2. Delay in Refunds:

Despite policy rules, in-practice delays happen in refund processing.

3. Lack of Awareness:

Most suppliers are not aware of the benefits of deemed export and lose out on entitlement claims.

Efficient consulting and documentation can overcome these problems easily.